Built for all: A global framework for building inclusive economies

The pandemic presents the opportunity to build a better future that supports inclusive growth, sustained prosperity, equal participation, and responsible stewardship.

It’s been over eighteen months since people around the world first got acquainted with the words “stay at home order” and “social distancing.” Human contact suddenly became dangerous and in the following months, the pandemic would expose our frayed social contract and deeply rooted inequities. However, it has also left governments with a clear imperative: we cannot return to “normal” because normal wasn’t good enough. So now begins the hard work of creating meaningful, lasting change. As we vaccinate citizens around the world, the road to a true recovery will take an unprecedented commitment from every sector and industry if we are to reimagine an economic system and society that creates dignity, fairness and equity.

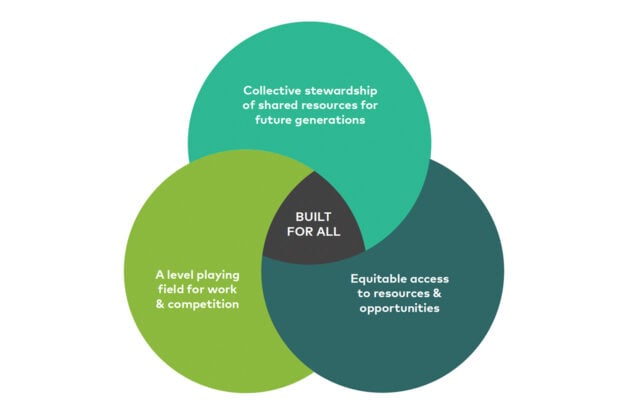

The Mastercard Center for Inclusive Growth and the Centre for Public Impact led a collaborative exercise over six months to understand the shortcomings of current economic systems and identify the core tenets of a new, inclusive economy. Research on the subject included an extensive literature review and discussions with Nobel laureates, heads of international organizations, and some of the world’s leading thinkers across sectors. The resulting Built for All framework for an inclusive economy reflects a proposal around which governments, civic sectors and businesses could align to build economies, which are designed to prioritize the flourishing of all people and the planet.

Here are four key takeaways from the experts involved on how to tackle the important work ahead.

Expand the measures of economic success

For years, we assumed if the economy was growing and the gross domestic product (GDP) expanding, all was well. But we know now that aggregate measures like GDP only capture the big picture and miss the lived experience for too many.

“GDP only gives you one important dimension: rising outputs that grow incomes at the aggregate level,” said Nobel laureate Michael Spence, senior fellow at the Hoover Institution. “It doesn’t tell you about the distribution of income or assets and value creation. It doesn’t tell you about individual and social well-being, health or economic security.”

Broad measures like GDP also miss the warning signs that some people and places are enjoying a bigger piece of the pie than others, which has been happening for more than a decade in the United States. Between 2010 and 2014, the U.S. created 104,600 net new firms yet a mere five metro areas were responsible for half of that increase. Nearly 20 years earlier, 30 metro areas shared the growth across all corners of the country.

“This concentration of opportunity leads directly to compounding inequality. Places left behind struggle to provide needed services and supports, and residents have fewer opportunities to migrate”, said Homi Kharas, senior fellow and deputy director for the Global Economy and Development program at Brookings, trapping them in a vicious cycle of lost opportunity. In the United Kingdom, people who moved to more successful job markets were 2.5 times more likely to earn higher wages than those who stayed behind.

Redesign systems that reinforce and perpetuate inequity

When we think of the systems in our society that are perpetuating inequality, we rarely think of competition. But competition (or lack of it) can be a driving force behind exclusion.

“We thought that competition would lead to less discrimination in the market,” said Jonathan Morduch, professor of public policy and economics at New York University, “but we are seeing competition that has reinforced existing discrimination and power structures.”

As a start, governments can play a role in creating a fair playing field on which to compete. When wealth concentrates at the top in either families or companies, it stifles competition and creates distrust that the game is rigged. A fair playing field instead creates the means to achieve financial security and the ability to act on opportunity, and through that comes inclusive growth.

“I think it’s important to talk about the means to achieve inclusive growth,” said Laura Tyson, former chair of the U.S. president’s Council of Economic Advisers and a professor at University of California at Berkley’s Haas School of Business. “That’s where I start with inequality of opportunity. Income inequality generates opportunity inequality, and opportunity equality is something you need for inclusion.”

Professor Tyson, – together with speakers including the former Chief Economist of the World Bank, Kaushik Basu, and Columbia University’s Jeffrey Sachs – will discuss how to embed fairness and sustainability into our economic systems at The Equity Imperative virtual event next week.

Opportunity doesn’t just happen. When the market in which ideas hatch and businesses grow is tilted toward those with the most capital and advantage, the result is a system that benefits only some.

“Today’s overconcentration of wealth at the top is not a matter of redistribution. We need to reform the market structure itself,” said Gabriela Ramos, assistant director-general for social and human sciences at UNESCO. Ramos cites the steadily declining start-up rates are a warning sign of this competitive imbalance. Case in point: only 200 firms are working on one of the most life-altering advances, artificial intelligence. “It’s dangerous to have so few firms working on technology that will have large societal consequences,” she warned.

Create incentives for long-term investment

Short-term thinking is no longer sustainable in the face of global and generational issues like climate change. A shift to longer-term planning will require new incentives such that the purpose of business, “is not to produce profits, but to produce profitable solutions to the problems of people and the planet,” said Colin Mayer, professor of management studies at Oxford University.

“Creating those incentives is where the public sector can help,” said Leora Klapper, lead economist in the finance and private sector research team at the World Bank. “Businesses provide employment, create profits and pay wages. In response to growing calls for a more inclusive economy, the public sector can set up rules and regulations for businesses to follow, which will incentivize more inclusive practices within a democratic society.”

Targeted incentives can also nudge financial systems to broaden their market and bring more lower-income and underserved people into the financial mainstream with appropriate products and services – along with consumer protections – that meet all customers’ unique needs.

Rebuild trust in institutions

Unfair competition and a fraying social contract have been contributing to a long slide in people’s trust in institutions. In the U.S., trust in government has been declining for a decade or more, as has trust in institutions like public schools and the Supreme Court, according to Gallup polls.

“Public and private institutions facilitate people’s social and economic lives,” said Ida Rademacher, vice president of the Aspen Institute, “but the erosion of social capital and the current mistrust in these institutions is proving to be a barrier to inclusion.”

To rebuild trust in communities, it is critical that inclusive recovery efforts be co-created at the local level to ensure long-term success. Trusted institutions can help bringing all sectors together and build bridges.

To learn more about Built for All and help shape the movement for a stronger global economy, please join the authors at The Equity Imperative: Building Sustainable and Inclusive Economic Systems held in partnership with the United Nations Development Programme.

What Role for Fintech in Driving Financial Inclusion In The Developing World?

About Knowledge Partner Mastercard

Related Posts

2 Comments

Leave a Reply

Public schools in England is the name for fee paying schools.

Public Schools in Scotland is the name for publicly funded schools (fee paying schools are called private schools).

Using the term “public schools” creates ambiguity.

Are the world bank are the used car salesmen of the financial world? OR are they more like the mafia? its hard to decide how to view them.