The Celtic tiger awakens: lessons from Ireland’s ‘weird economy’

The fallout of the financial crisis silenced the roars of Ireland’s ‘Celtic tiger’ economy. Now it’s back, its growth – and its growing pains – offer useful lessons for other small, rapidly-developing countries. At the Global Government Finance Summit, its finance department chief economist John McCarthy profiled the country’s ‘weird economy’

“Sustainable development and new digital technologies could be complete game-changers,” said Noureddine Bensouda, general treasurer of the Kingdom of Morocco. “On one hand, they provide broad opportunities for positive transformation of economies and societies; on the other, they’re changing faster than our capacity to adapt, and can perpetuate existing inequalities.”

Introducing the 2023 Global Government Finance Summit – an annual gathering of finance department and treasury leaders, hosted this year in Rabat by the Moroccan government – Bensouda pointed to a set of “increasingly complex, diverse and interconnected” global challenges. Civil service finance leaders have a crucial role to play in equipping their countries to survive and thrive, he said: “We must ask ourselves how public finance can adapt to this new era: governments and financial institutions must not only transform their approaches, but also harness the potential of digitalisation and sustainability.”

At the Summit’s four daytime sessions, the civil service leaders – who hailed from 12 countries on five continents – would explore these issues in wide-ranging discussions. But the event began with an after-dinner presentation by John McCarthy, the chief economist of Ireland’s Department of Finance, who profiled his country’s “weird economy”. Small, open, and radically transformed over the last 20 years, Ireland illustrates both many of today’s opportunities, and several of its risks – making it something of a canary in the economic mine.

From farming to pharmaceuticals

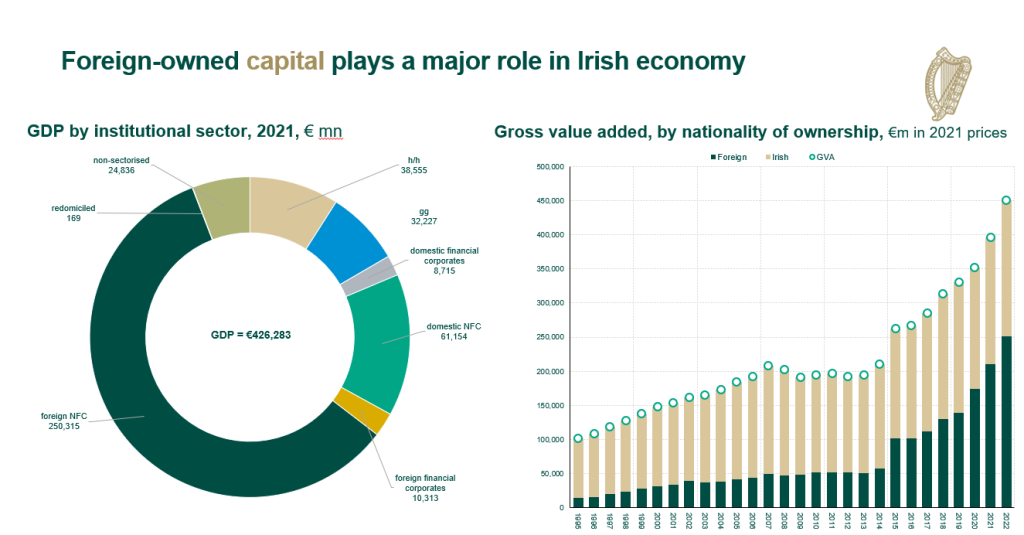

Since Ireland joined the European Economic Community half a century ago, McCarthy said, agriculture’s contribution to GDP has dropped from 15% to just 1%; the proportion of workers employed on the land has meanwhile fallen from 25% to 5%. Unlike many nations in the developed world, however, Ireland has seen a rise in manufacturing: industrial employment may have dipped from 30% to 20% of the workforce, but its contribution to GDP has risen from 35% to 40%.

“Stuck in the mid-Atlantic and with a very small domestic market, we can’t have a comparative advantage in heavy manufacturing,” he explained, “so for 50 years, the authorities have been targeting sectors whose exports are high value-added but physically lightweight.” The country has attracted huge foreign investments, particularly by pharmaceuticals and IT firms: the proportion of GDP generated by overseas businesses has grown from 20% to more than 50% over the last 25 years.

Ireland’s generous corporate tax regime has been helpful here – though McCarthy argued that its effective rate of taxation is close to its competitors’ (see our forthcoming report on the Summit’s taxation session). But equally important is its increasingly highly-educated population: following a rapid expansion in higher education, more than half of 25-year-olds now have a degree. “We’re seeing an increase in human capital working its way through the labour force,” he explained. “That’s how we’ve been able to transform the labour market from low value-added and agriculture.”

Concentrating hard

Ireland’s development model is not, however, without its risks. Having “concentrated economic activity within a small number of sectors and a small number of firms,” the country is highly dependent on a handful of big investors: half a dozen companies produce most of Ireland’s goods exports. Corporate tax revenues may have risen from €4bn (US$4.3bn) to €24bn (US$25.5bn) in a decade, said McCarthy, but “the vast majority of that is down to 10 firms”. And he’s only too aware of how big corporates can fall as quickly as they rise.

“At its peak, Nokia accounted for something like 3% of Finland’s GDP; now I don’t know anyone with a Nokia phone. In a world where technology is changing so rapidly, today’s high-tech, cutting-edge global leader could be redundant in a couple of years’ time.”

Asked whether the government is trying to broaden its economic base, McCarthy replied that “as a small economy, we can’t diversify that much: we have to develop comparative advantage in a relatively small number of sectors”. Nonetheless, civil servants have been working both to build links between the foreign-owned sector and Irish SMEs, and to embed multinationals more deeply in the Irish economy – offering R&D tax credits, for example, in a bid to capture a broader swathe of their activities.

Meanwhile, inside government McCarthy and his colleagues are “trying to minimise the risk that what we see as windfall revenue gains are used to fund permanent fiscal commitments – either expenditure increases or tax reductions”. The taxes paid by major foreign investors, he suggested, could be paid into a sovereign wealth fund – creating a nest egg for future generations of Irish people, while avoiding structural dependence on a revenue stream that is vulnerable to changes in technologies and markets.

Too many jobs, not enough homes

Alongside inward investment and education, Ireland owes some of its economic success to rapid immigration: since 2000 the proportion of foreign-born workers has shot up from 5% to 20%. Yet despite this inflow, a rapid post-pandemic recovery – which has left employment levels 10% above their pre-pandemic peak – has pushed unemployment rates down to an unprecedented low. “By any reasonable definition, we’re at full employment,” said McCarthy.

In part, this is because Ireland – unlike countries such as the UK and US, which have experienced a ‘big quit’ in the wake of the pandemic – has seen rising labour market participation rates. There’s little hard data to explain this divergence, said McCarthy; but Ireland’s relatively young population may suffer less from the lingering effects of COVID, while rates of remote working have remained elevated since the pandemic – having risen 15 points to about a third of the workforce. Changed attitudes to flexible and remote working, McCarthy speculated, may be allowing more women to return to the workforce after having children.

The rapid changes in Ireland’s economy have “transformed living standards over the past couple of decades,” concluded McCarthy – but the country now faces four slow-moving but inescapable challenges, which he summarised as the “four Ds”. Alongside decarbonisation and digitalisation (covered in forthcoming reports on the Summit’s sustainability and data sessions), demographic issues and deglobalisation represent significant threats to future growth.

On the demographic side, the country isn’t building enough homes to meet the demand created by rapid immigration. The population has risen by 8% in just six years, but housebuilding never recovered after Ireland’s 2008 housing crash: “A lot of construction workers exited the market then, and they’re not coming back,” McCarthy explained, adding that the planning system represents another barrier to construction.

Having dropped by half between 2008 and 2012, house prices returned to their 2008 peak in 2021 – stoking new social tensions. “There was absolutely no problem with immigration until about five years ago, when some of the constraints in the housing market really began to become very binding,” he said. “But there is some pushback now beginning to emerge from small portions of the population.”

Releasing the choke points

Without continued immigration, however, Ireland may struggle to support a rapidly ageing population: the ratio of working people to retirees is expected to fall from 4:1 to 3:1 over the next 12 years, dropping exponentially thereafter. “Demographically-sensitive spending is set to ramp up very, very quickly,” McCarthy warned. “Between 2020 and 2030, we will have to pay an additional 3% of national income every year simply to maintain the status quo” in spending on pensions and public services.

Finally, indicators of worldwide deglobalisation track an uncomfortable trend for trade-based economies such as Ireland’s. It’s not yet clear that the long shift towards ever more integrated global supply chains has really gone into reverse, said McCarthy; but the pandemic and Ukraine war have certainly exposed “choke points: single points of failure” that illustrate a “need to improve security of supply. Given that Ireland is highly integrated into global value chains, this is something that we’re thinking about a lot”.

Summarising, McCarthy identified Ireland’s strengths as its openness – to goods, services, capital and labour – and the ease of doing business: “Red tape is relatively limited in Ireland,” he said. On the weaknesses side, he named poor productivity in some public services, dependence on carbon-intensive energy sources, infrastructure gaps, and low productivity among domestic businesses.

Naming the country’s economic opportunities, he picked out energy – Ireland is well placed to harness the power of wind and wave – and the OECD’s Base Erosion and Profit Shifting (BEPS) initiative, which he hopes will strengthen “tax certainty”. Turning to threats, he added a fifth ‘D’: dependence on a few global firms, and on UK markets – newly impeded by post-Brexit frictions – as the destination for many more traditional exports, such as food.

All these issues would lie at the heart of the finance leaders’ discussions over the following day, with sessions covering sustainable growth, data and digitalisation, tax reform, and the state’s role as a buyer and commissioner. As Bensouda said, finance departments have a responsibility to “accelerate the momentum towards a sustainable and equitable world which leaves nobody behind” – reshaping economies and retooling workforces for the challenges ahead. “Words are important, but it’s incumbent upon all of us to walk the talk in our commitments and in their implementation,” Bensouda concluded. The Global Government Finance Summit would explore exactly what that means for this generation of finance leaders – and for the next.

This is the first report on the Global Government Finance Summit held in Rabat, Morocco in June 2023, covering Irish finance department chief economist John McCarthy’s analysis of his country’s economic strengths and weaknesses. Further reports will be published here soon.

To ensure that participants feel able to speak freely at the Summit, we give all those quoted the right to anonymise, edit or delete their comments before publication.

About Matt Ross

Matt is Global Government Forum's Contributing Editor, providing direction and support on topics, products and audience interests across GGF’s editorial, events and research operations. He has been a journalist and editor since 1995, beginning in motoring and travel journalism – and combining the two in a 30-month, 30-country 4x4 expedition funded by magazine photo-journalism. Between 2002 and 2008 he was Features Editor of Haymarket news magazine Regeneration & Renewal, covering urban regeneration, economic growth and community development; and from 2008 to 2014 he was the Editor of UK magazine and website Civil Service World, then Editorial Director for Public Sector – both at political publishing house Dods. He has also worked as Director of Communications at think tank the Institute for Government.

Related Posts